The Bank of Canada has just announced a 0.50% increase in their overnight rate, bringing it to 1.50%. What does that mean for your mortgage? If you are a fixed-rate mortgage holder, you aren’t directly impacted by this increase, but fixed rates are also currently on the rise. If you have a fixed-rate mortgage you will be sheltered from rate increases until your mortgage term is complete. If your mortgage maturity date is nearing, though, it may still be worth your while to explore your rate options now, by weighing your prepayment penalty versus the projected rate increases you would encounter by waiting for your maturity date. While this is important to note, fixed rates aren’t the focus of this blog. Today, we will be focusing on variable interest rates, and how the overnight rate increase will impact those associated mortgages.

So, what exactly does a 0.50% increase to the overnight rate mean? This means that the prime rate will increase by 0.50%, bringing it from 3.20% to 3.70%. The prime rate is the interest rate that banks offer borrowers. You will be offered a discount or addition to prime, depending on the mortgage type, and overall strength of your mortgage application. So, if you have a variable rate, your rate will change as prime fluctuates, but the rate discount you received from your lender will be locked in. For example, If you have a discount of 0.50% off of prime, your rate would be 3.70%(prime) – 0.50% (your discount) = 3.20%.

Here are a few examples of different mortgage amounts, and the impact of prime changes to their corresponding payments:

Rate Increase Example #1

Example one involves a mortgage of $500,000 with a discount on prime of 0.50%. Before this most recent rate increase, you would be receiving an interest rate of 2.70% (3.20% prime – 0.50% rate discount), and paying a monthly obligation of $2,698.50 based on a 20-year amortization. After this increase, the new rate would be 3.20% (3.70% prime – 0.50% rate discount) with a corresponding monthly obligation of $2,823.31. This is a $124.81 monthly payment increase.

Rate Increase Example #2

Example two involves a mortgage of $200,000 with a discount on prime of 0.30% before the most recent rate increase. This would have resulted in an interest rate of 2.90% with a payment of $1,099.21 (20-year amortization). After this increase, the rate they would be paying is 3.40% bringing their payment to $1,149.67.

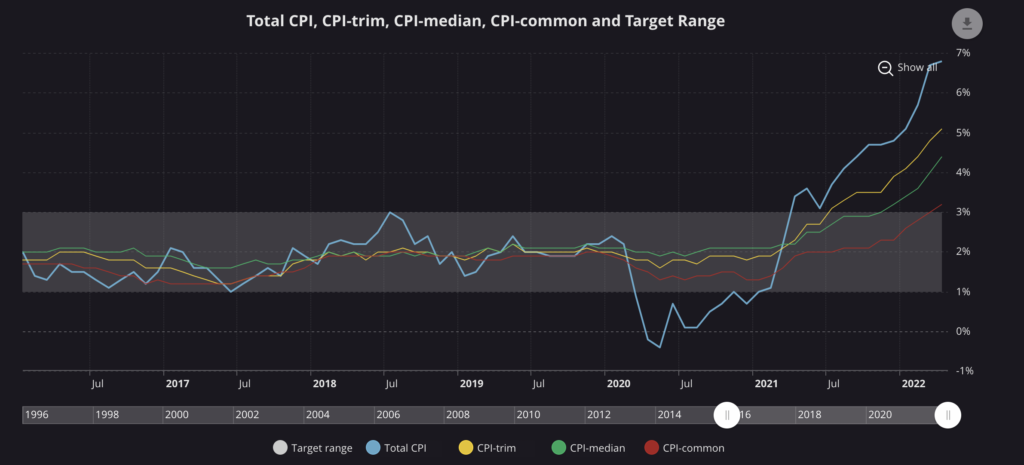

The goal of the Bank of Canada’s overnight rate increases is to better control inflation. In April of 2022, the CPI reached a high of 6.8%. The Bank of Canada is trying to decrease this figure to a target of 1%-3%.

A recent article released by the Bank of Canada stated the following:

“Inflation globally and in Canada continues to rise, largely driven by higher prices for energy and food. In Canada, CPI inflation reached 6.8% for April – well above the Bank’s forecast- and will likely move even higher in the near term before beginning to ease.”

Bank of Canada

The overnight rate is the primary tool used by the Bank of Canada to control inflation. It is predicted, then, that the overnight rate will continue to increase this year.

“The increase in global inflation is occurring as the global economy slows. The Russian invasion of Ukraine, China’s COVID-related lockdowns, and ongoing supply disruptions are all weighing on activity and boosting inflation. The war has increased uncertainty and is putting future upward pressure on prices for energy and agricultural commodities.”

Bank Of Canada

It is hoped that the factors attributing to the increased inflation rates will be short-lived, and the upward pressure to control inflation will cease.

When Will The Bank of Canada Stop Raising Rates?

Unfortunately, there is no way of knowing for certain when the economy will be more prosperous, or rates will cease to increase. As the leading factors contributing to the raising rates are global, and not localized, there is decreased Canadian control over the situation. Once inflation decreases to the desired 1%-3% range, though, you can anticipate that the Bank of Canada will begin decreasing its rates again.

Hopefully, this blog helped give you a better understanding of this recent rate increase and why rates are on the rise. If you have any questions don’t hesitate to call my office at 519-250-4848 or email me at [email protected].

{kind=link}

{kind=link}