Tips for First-Time Homebuyers

Although mortgage debt is ‘smart’ debt, buying your first home is a huge financial decision and there is a lot to think about. It’s one of the most important financial decisions most Canadians will make in their lifetimes. Here are five tips to help you get off on the right foot in your home buying journey.

Determine what you can afford

Before you start shopping for a home – and long before you consider putting an offer on one – build a realistic budget. Remember that home-ownership involves costs beyond the monthly mortgage payment such at utility bills, insurance, taxes, and home upkeep. Consider opportunities that will help you manage your housing costs. Perhaps you could rent out part of your home, or have a roommate to help offset expenses. Or if you are in a condo, possibly rent out an extra parking space if you have one.

Start off small

The dream house may be priced too high, so a starter home might be the right option. A smaller home or maybe a house just outside of the expensive area will help get a foot in the door. You can take advantage of today’s low interest rates to pay off the home quicker and use the equity from the first home to buy that dream home later.

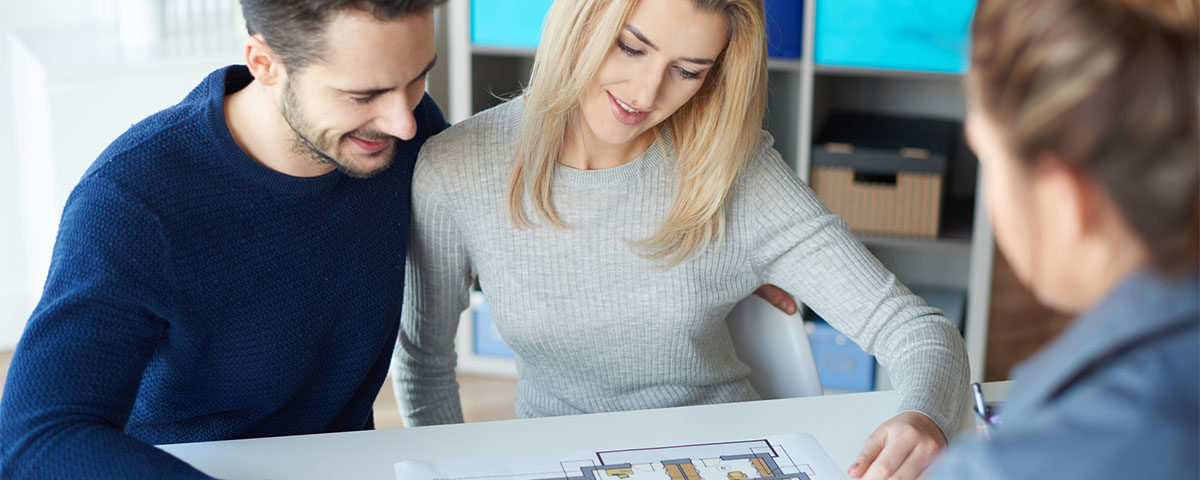

Get expert advice

Work with a mortgage broker to sort through all of the mortgage options and get the right combination of mortgage features, privileges and rate that is best matched to your needs. The right mortgage goes beyond just the rate; it’s important to also consider term, prepayment options, refinancing penalties, restrictions, and fees. We’d be happy to help you build a strong away team so that all aspects of your home buying experience are efficient and professional. Your team will include a realtor, lawyer, and a home inspector.

Plan for closing costs

There are additional costs that come with buying a home, including lawyer fees, reimbursements, land transfer or similar tax, appraisal, home inspection, and title insurance. So, you’ll need to have some extra funds set aside to cover these costs. Generally, you can expect to pay between 1.5 per cent and 4 per cent of the home’s selling price in total closing costs.

Accelerate your payments – early and often

A mortgage is the largest debt you will probably ever take on, and paying it down faster can mean large savings on interest costs over the long-term. Get in the habit of making lump sum payments whenever possible, and consider making bi-weekly payments as a way to decrease the life of the loan. We can also provide strategies to help you pay your mortgage off faster and shave thousands off interest costs.

There’s so much to consider. Working together, you can get into the market and start your wealth building with smart debt! We look forward to helping you achieve your dream of home-ownership!

Thank you for taking the time to read our blog. Be sure to like us on Facebook for regular news and updates.

Rasha Ingratta & Mortgage Associates

By Mortgage Intelligence

® Registered trademark of Mortgage Intelligence Inc. © Copyright 2013, Mortgage Intelligence Inc., all rights reserved.

{kind=link}

{kind=link}

{kind=link}